Market News

Data & Statistics

Listed Companies

Equities, Debt, Funds

Derivatives

Rules & Trading Participants

Systems

Self-Regulation

Clearing & Settlement

![]() Close

Close

Market News

Data & Statistics

Listed Companies

- Company Announcement Service

- Listed Company Search

- Corporate Governance Information Search

- Number of Listed Companies/Shares

- New Listings/ Transfers/ Delistings

- Market Alerts

- Measures against Listed Companies

- Other Information

- Earnings Announcements/ Annual General Shareholders Meetings

- Introduction of Listed Companies

Equities, Debt, Funds

Derivatives

Rules & Trading Participants

Systems

Self-Regulation

Clearing & Settlement

- For Individual Investors

- For Listed Companies

- For Prospective Issuers

- For Trading Participants

- For Institutional Investors

- For Media

Recommended Contents

- TSE Daily Report

- Daily Report

- Equities Market Summary

- Stock Price Index - Real Time Values

- Daily Publication, etc., Concerning Margin Trading

- Regulatory Measures, etc., Concerning Margin Trading

- Short Selling Value

- Special Quotations

- JPX Monthly Headlines

Our Markets

Featured Products

- Stocks (Domestic)

- ETFs

- REITs

- TOKYO PRO Market

- TOKYO PRO-BOND Market

- Nikkei 225 Futures (Large Contracts)

- TOPIX Futures (Large Contracts)

- 3-Month TONA Futures

- Nikkei 225 mini Options

- Gold Standard Futures

- Platts Dubai Crude Oil Futures

External Links

Equities, Debt, Funds

Listing (Domestic Stocks)

Listing

Continued Listing Criteria

Delisting Criteria

Code of Corporate Conduct

Enforcement Measures

Timely Disclosure System

Enhancing Corporate Governance

Independent Directors/Auditors

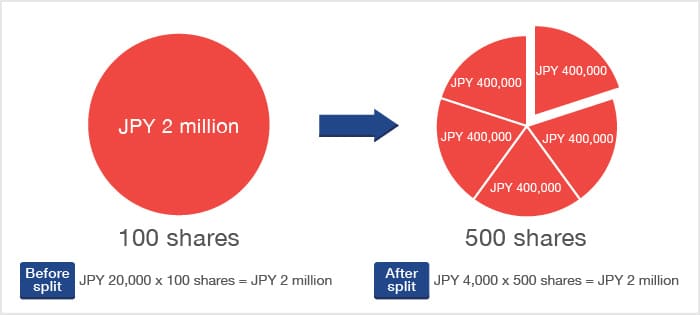

Reduction of Investment Unit / Mechanism and Effects of Share Split

Listing Fees

![]() Close

Close