Interest Rate SwapClearing Fund

Clearing Fund for IRS

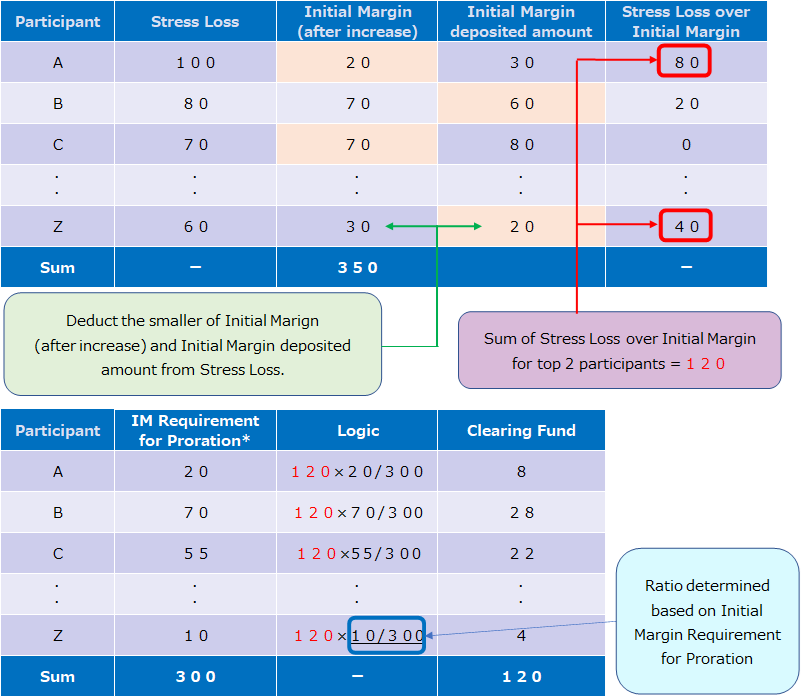

On the each business day, the portion of the the amount of loss (risk equivalent under stressed conditions) that may arise under extreme but plausible market conditions (stressed condition) exceeding the smaller of the amount of Initial Margin and deposited Initial Margin (excess risk amount) is calculated with respect to the positions of each IRS Clearing Participant as of 19:00 on such day. The required amount of clearing fund shall be the amount equivalent to the expected loss arising at the time of simultaneous default of two IRS Clearing Participants (including their Affiliated Companies(*1)) whose excess risk amounts are the largest and the second largest, prorated according to the Required Initial Margin Amount of each IRS Clearing Participant (calculated on assumption that no add-on according to credit condition or based on Net Capital is applied) (if such amount is less than 100 million yen, then the minimum clearing fund requirement shall be100 million yen).(*2)

(*1) Any subsidiary or affiliate, or the parent company of such Clearing Participant, or any subsidiary or affiliate of the parent company.

(*2) The total required Clearing Fund for IRS amount contributed by all Clearing Participants was JPY 20.6B (as of 30, Jun, 2026)

Illustration of Clearing Fund

* IM Requirement for Proration is exclusive of add-on according to credit condition or based on Net Capital

Stress Scenarios to be Used for Calculation

Stress scenarios are set by using Principal Component Analysis and historical scenarios. Expected amount of losses that may arise on the part of each Clearing Participant will be calculated with respect to these stress scenarios (the risk equivalent under stressed conditions).