Search results 5071-5080 / 10648

- sort:

- relevance

- latest

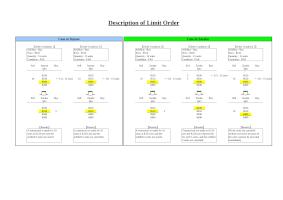

Sell/Buy : Buy Sell/Buy : Buy Sell/Buy : Buy Sell/Buy : Buy Sell/Buy : Buy Price : 8510 Price : 8510 Price : 8510 Price : 8520 Price : 8510 Quantity : 15 units Quantity : 15 units Quantity : 15 units Quantity : 15 units Quantity : 15 units Condition : FAS Condition : FAK Condition : FAS Condition : FAK Condition : FOK Sell Itayose Buy Sell Itayose Buy Sell Zaraba Buy Sell Zaraba Buy Sell Zaraba Buy MO MO MO MO MO …………… 8520 8520 8520 5 8520 ←LO : 15 units 8520 10 8510 ←LO : 15 units 10 8510 ←LO : 15 units 10 8510 ←LO : 15 units 5 8510 10 8510 ←LO : 15 units 8500 8500 8500 8500 8500 8490 8490 8490 8490 8490 …………… Description of Limit Order Case at Itayose Case in Zaraba 【Order Condition 1】【Order Condition 2】【Order Condition 3】【Order Condition 4】【Order Condition 5】 Sell Zaraba Buy Sell Zaraba Buy Sell Zaraba Buy Sell Zaraba Buy Sell Zaraba ...

1 Concerning the Partial Prohibition of Order Cancellations Prior to Call Auctions in Closing Auction of the Day Session 1 Applicable Products Nikkei 225 Futures (All contract months of large, mini and micro) TOPIX Futures (All contract months of large) 2 Applicable Time Periods One minute prior to closing auction of the day session (15:45) (the remaining call auctions shall have NCP, so will be not applicable) 3 Actions Principally Prohibited (1) Cancelling sell orders at or lower than the equilibrium price (the expected call auction crossing price based on available orders at that time; hereinafter, EP) and cancelling buy orders at or higher than the EP or altering a sell order from a price at or lower than the EP to a price higher and altering a buy order from a price at or higher than the EP to a price lower. Such orders need to have a ...

Itayose Conditions and Pricing Examples Cond. 1 2 3 In the case where there are two or more prices that meet Condition 2, the price at which the difference between the cumulative volume of sell orders and the cumulative volume of buy orders (hereinafter referred to as "imbalance") is the smallest. In the case where there are two or more prices that meet Condition 1, the price at which there will be maximum traded volume. The price where bids and offers match that is between one tick above the highest order price and one tick below the lowest order price*1. 5 One of the following prices: 1) In the case where the highest price among the prices at which the imbalance (if there are several prices at which there are imbalances on both sell and buy sides, it shall be limited to the lowest price among the prices at ...

(Provisional English Translation) Demutualization Framework of Japan Securities Depository Center (JASDEC) November 2, 2001 Committee for Reform of Securities Clearing and Settlement System Japan Securities Dealers Association -1- Demutualization Framework of Japan Securities Depository Center November 2, 2001 Committee for Reform of Securities Clearing and Settlement System Items Description Remarks 1.Basic Management Policy (1) Basic Management Policy (2) Basic Financial Policies ○The basic management policy to be taken by the new company is to contribute to improving the functions of securities market by providing a highly secure, efficient and convenient infrastructure for the clearing and settlement of securities, and to contribute to the further development of the national economy by enhancing international competitiveness of the securities market, taking into account the matters below; ①Operating businesses that meet the needs of users of the securities depository and book-entry transfer system through direct governance by participants as its shareholders ...

Interim Report of the Committee for Reform of the Securities Clearing and Settlement System (Memorandum) Note: This is a tentative translation of the "Memorandum of the Interim Report of the Committee for Reform of the Securities Clearing and Settlement System " and has not been formally approved by the issuer of the report. The translation, prepared by the secretariat of the JSDA, is intended to facilitate understanding of the reform by the international audience. March 31, 2000 I. Introduction A securities clearing and settlement system superior in security, productivity, and efficiency is a basic infrastructure for securities markets. It is one of the most important issues yet to be tackled in Japan’s efforts to establish an internationally competitive financial center. In light of the globalization of securities transactions and worldwide competition among markets, major Western countries have already adopted "DVP" (Clearing versus Payment) for a wide range of securities, and ...

1 Development of Comprehensive Improvement Program for Listing System June 22, 2006 Tokyo Stock Exchange, Inc. Tokyo Stock Exchange, Inc. (TSE) considers that important duties of a securities exchange are enhancing investors’confidence in the market and strengthening its competitiveness in global markets, by promoting harmonization between vigorous corporate actions of listed companies and investors’ protection. Last March, TSE announced“Discussion Paper on Improvements to the Listing System”which finalized basic matters to be studied as measures so as to achieve these goals. TSE absorbed a wide range of valuable opinions on the discussion paper from investors and market users at home and abroad. Taking these opinions into account, TSE formulated“Development of a Comprehensive Improvement Program for the Listing System”as follows which are basic action guidelines to improve its listing system in the future. 1.Basic Thoughts (1) Basic Policy Soundness of the market can be ensured if ...

- 1 - Reference Translation Updated Consolidated Results of Independent Directors/Auditors Notifications July 21, 2010 Tokyo Stock Exchange, Inc. Tokyo Stock Exchange, Inc. (“TSE”) hereby announces the updated consolidated results of the independent directors/auditors notifications. This results were compiled in conjunction with the enforcement1 of the provision in TSE regulations (Rule 436-2 of the Securities Listing Regulation) which requires each listed company to secure at least one independent director/auditor (hereinafter“ID/A”) (meaning an outside director/auditor who is unlikely to have conflicts of interest with general shareholders; the same shall apply hereinafter). The provision shall be applied to each listed company from the period after it settles accounts in or after March 2010. 1. Independent Directors/Auditors Notifications These consolidated results are based on ID/A notifications which were submitted by July 16, 2010 by domestic companies listed as of June 30, 2010 (2,301 companies) (...

https://www.jpx.co.jp/english/equities/improvements/general/tvdivq0000004iib-att/action_plan2009.pdf

57KBReference Translation DISCLAIMER: This translation may be used only for reference purposes. This English version is not an official translation of the original Japanese document. In cases where any differences occur between the English version and the original Japanese version, the Japanese version shall prevail. Tokyo Stock Exchange Group, Inc., Tokyo Stock Exchange, Inc., and/or Tokyo Stock Exchange Regulation shall individually or jointly accept no responsibility or liability for damage or loss caused by any error, inaccuracy, or misunderstanding with regard to this translation. 1 Listing System Improvement Action Plan 2009 September 29, 2009 Tokyo Stock Exchange, Inc. <Introduction> The Tokyo Stock Exchange (TSE) intends to pursue a comprehensive revision of the listing rules from the perspective of the proper fulfillment of secondary market functions, and our role in supporting listed companies with improving corporate value and global competitiveness, while protecting and valuing investors. In order to achieve this, ...

- 1 - Reference Translation Consolidated Results of Independent Directors/Auditors Notifications May 20, 2010 Tokyo Stock Exchange, Inc. The Tokyo Stock Exchange, Inc. (“TSE”) hereby announces the consolidated results of the independent directors/auditors notifications. The TSE requested listed companies to submit these notifications by March 31, 2010. 1. Independent Directors/Auditors Notifications The TSE partially revised the Securities Listing Regulations, etc. on December 30, 2009. The revision consisted of including a provision to the effect that a listed company must, for the purpose of protecting general shareholders, secure at least one independent director/auditor (hereinafter“ID/A”) (meaning an outside director/auditor who is unlikely to have conflicts of interest with general shareholders; the same shall apply hereinafter) as“Matters to be Observed”in the Code of Corporate Conduct (Rule 436-2 of the Securities Listing Regulations). This provision shall be applied to each listed company from the day ...

(Reference Translation) - 1– DISCLAIMER: This translation may be used only for reference purposes. This English version is not an official translation of the original Japanese document. In cases where any differences occur between the English version and the original Japanese version, the Japanese version shall prevail. Tokyo Stock Exchange, Inc., Tokyo Stock Exchange Group, Inc. and/or Tokyo Stock Exchange Regulation shall individually or jointly accept no responsibility or liability for damage or loss caused by any error, inaccuracy, or misunderstanding with regard to this translation. Summary of Deliberations on“Listing System Improvement Action Plan 2009 (Matters to consider for actual implementation)” March 31, 2010 Tokyo Stock Exchange, Inc. Advisory Group on Listing System Improvement The Advisory Group on Listing System Improvement (hereafter the“advisory group”) was established by Tokyo Stock Exchange, Inc. (hereafter the“TSE”) in September 2006 for the purpose of improving the listing system based on ...