FAQ (Equities)

Listed Company

- Q1. How can I view the disclosure information on financial results?

-

A1.

Disclosure information on financial results is on the following two websites:

- Company Announcements Service

- Listed Company Search

- Information may only be available in Japanese.

- Company announcements in English may be released later than those in Japanese or summarized.

- Company Announcements Service

Information from companies will be published at same time as it is disclosed.

Click the button below to use the service.

Company Announcements Service

(Main Contents)- The service provides company announcements by listed companies, which include material information for investment decisions.

- Information from companies will be published at same time as it is disclosed.

- Information is available for a period of 31 days (including the date of disclosure, weekends, and holidays)

- Listed Company Search

TSE offers a "Company Search" for TSE-listed companies through which investors can access disclosure information on financial results of the companies in the past five years.

Click the button below to use the service.

Listed Company Search

(Contents)- Information is sorted by company.

- Information on “Listed Company Search” is updated around 1:30 a.m. every day.

- To view the user guide, please click the link below.

User Guide of Listed Company Search

- Q2. I’d like to know how to use "Stock Data Search”.

-

A2.

Please refer to the following link for user instructions.

Stock Data Search (User Guide)- "Stock Data Search" is designed to search TSE listed companies.

Listing Rules

- Q1. If I hold shares in a company that stops meeting the continued listing criteria, will they be delisted?

-

A1.

If a company stops meeting the continued listing criteria, it will enter an improvement period. If it still does not meet the criteria within the improvement period, it will be designated as a Security Under Supervision or Security to Be Delisted, and will subsequently be delisted.

In addition, a company that stops meeting the continued listing criteria is required to disclose, within three months, a plan describing its measures to meet the criteria and the schedule for their implementation. For examples of schedules and other details, please refer to this page and check each criterion.

Details of Continued Listing Criteria

- Q2. If a bidder announces a takeover bid (TOB) for shares I hold, and the stock is designated as a Security Under Supervision, will the stock be delisted? Also, if I do not tender my shares and the stock is delisted, what will happen to my shares?

-

A2.

After a stock is designated as a Security Under Supervision, if the TOB is successful and TSE determines that the stock meets the delisting criteria, the stock will be designated as a Security to Be Delisted and will subsequently be delisted.

However, if the tender offer is not successful, the stock’s designation as a Security Under Supervision will be lifted.

If you do not tender your shares and the stock is delisted, in many cases the issuing company will purchase your shares for cash as part of a squeeze-out process. If the bidder is a listed company, it may also exchange your shares for shares issued by the bidder at a certain exchange ratio.

Please carefully review the opinion disclosed by the issuer of your shares regarding the takeover bid, as well as any subsequent timely disclosures.

- Q3. Please explain the revision of the continued listing criteria for the Growth Market.

-

A3.

The criteria will be revised as of the last day of the first fiscal year ending on or after March 1, 2030 as follows:

If a company does not meet the continued listing criteria as of the last day of the first fiscal year ending on or after March 1, 2030, it will be given a one-year "improvement period." If the company does not meet the criteria within this period, it will be delisted.

- Before the revision: Market capitalization of JPY 4 billion or more when the company has been listed for ten or more years

- After the revision: Market capitalization of JPY 10 billion or more when the company has been listed for five or more years

For details, please refer to the following page.- If a listed company discloses a conformance plan within three months of the last day of the first fiscal year ending on or after March 1, 2030, and said conformance plan covers a period beyond the last day of the first fiscal year ending on or after March 1, 2031, then the company will be allowed to remain listed until the end of said conformance plan.

Measures to Enhance the Functionality of the Growth Market

Trading of Domestic Stocks

- Q1. Is there any material that explains the trading rules, such as trading hours, prices, and the mechanisms of trading?

-

A1.

For information on the trading rules, please refer to the following page:

Trading Rules of Domestic Stocks (Overview)

On this page, you can find the "Guide to TSE Trading Methodology," which explains how trading on the TSE market works. A paper edition of this guide is also available for purchase.

- Q2. Please explain the short selling regulations.

-

A2.

The documents "Responses Pertaining to Comprehensive Revision to Short Selling Regulations" and "FAQ on Comprehensive Revision to Short Selling Regulations" are available on the following page.

Restrictions on Trading (Short Selling Restrictions)

- Q3. Please explain how TSE monitors the closing auction session in the cash market.

-

A3.

During the pre-closing session, if order prices are changed or orders are cancelled arbitrarily in a way that affects the expected matching price, it may reduce the predictability of the closing price, hinder smooth price formation, and even induce orders from other investors. Such actions may raise suspicions of closing price manipulation (unfair trading).

With the introduction of the closing auction session, we have established the "Guidelines Concerning Focused Monitoring of Order Changes in Closing Auction" and are conducting monitoring accordingly.

Strengthening the Functions of the Cash Equity Market

- Q4. Before the opening price was determined in the morning session, I placed a limit order at the same price as the opening price, but it was not executed. Why?

-

A4.

All orders received before the opening price is determined in the morning session are treated as "simultaneous orders."

Simultaneous orders at the same price are aggregated by securities company, not by individual order, and one trading unit is allocated to each securities company in turn in descending order of their total order quantities.

Here are some possible reasons in your case:For more details, please refer to Q15, Q16, and Q17 in the "Guide to TSE Trading Methodology." Please note that the same allocation method applies in cases where the closing price is determined by "closing auction at the limit price."- No unit was allocated to your securities company.

- Although your securities company received some units, the distribution to individual customers is determined by the rules set by the securities company. As a result, no units were allocated to you.

Trading Rules of Domestic Stocks (Overview)

- Q5. What measures are being implemented to lower investment units?

-

A5.

To create an environment in which individuals can easily invest, TSE asks listed domestic companies to make efforts to transition to and maintain an investment unit of less than JPY 500,000. For those with investment units of JPY 500,000 or more, TSE requests the following:

Reduction of Investment Unit

- Consideration of a share split to lower the investment unit

- Disclosure of the company’s approach and policy regarding the reduction of investment units.

Margin Trading

- Q1. What is the purpose of margin trading?

-

A1.

The role of a stock market is to provide investors with a place to buy or sell stocks. In order for the market to achieve this goal effectively, it should allow participants to execute trading at any time (high liquidity) and ensure fair and smooth price formation at all times.

In the market, there is real supply and demand from investors who have money or stocks for trading and speculative supply and demand from investors who do not have the money or stocks but want to trade. If speculative supply and demand is included in the form of margin trading in addition to real supply and demand, there will be greater transaction volume and diversity of investment decisions which could influence price formation in the market. As a result, this will likely improve market liquidity and further facilitate fair and smooth price formation.

- Q2. How can investors use margin trading and what advantages are there?

-

A2.

(Main uses)

(Advantages)

- Purchase stocks that are considered cheap

If an investor considers that the current stock price is relatively low and will rise, he/she can use margin trading to buy the stocks even if he/she does not have available funds. - Sale stocks that are considered expensive

If an investor considers that the current stock price is relatively high and will fall, he/she can use margin trading to sell the stocks even if he/she does not hold them. - Hedge selling

For example, though an investor may fear that the stock price will have fallen from the purchase price, he/she dosen't want to sell the stock for some reason. In order to hedge the risk of price decline, he/she can sell the stocks on margin trading.

(Disadvantages)- Enable investment at any opportune time

Margin trading can be used to invest at any time, for example, when an investor wishes to buy stocks now but has no funds available, or wishes to sell now but does not hold the stocks. - Save on investment funds

In margin trading, an investor does not have to prepare the full amount of funds or quantity of stocks to sell, but by depositing the amount of funds equivalent to 30% or more of the execution amount as "customer margin", he/she can buy or sell the stocks committing less funds (in an actual transaction, miscellaneous expenses besides customer margin will be required). Moreover, since the investor may use other securities in his/her portfolio as a substitute for customer margin, the investor can also manage his/her portfolio more effectively.

If actual stock price movement is different from what was expected, there is a risk of incurring loss in excess of the amount of customer margin. - Purchase stocks that are considered cheap

- Q3. What are the benefits of margin trading for listed companies?

-

A3.

In the market, there is real supply and demand from investors who have money or stocks for trading and speculative supply and demand from investors who do not have the money or stocks but want to trade. If speculative supply and demand is included in the form of margin trading in addition to real supply and demand, there will be greater transaction volume and diversity of investment decisions which could influence price formation in the market. As a result, this will likely improve market liquidity and further facilitate fair and smooth price formation.

Moreover, improved market liquidity will pave the way for new investors to participate in the market, which in turn will lead to reduced volatility in stock prices (due to more stable price formation).

- Q4. What is "standardized margin trading" and "negotiable margin trading"?

-

A4.

There are two types of margin trading. One of these is referred to as "standardized margin trading" in which premium charges (refer to Question 7), payment deadline, and treatment of rights in cases of subscription warrants are granted for a stock split, etc. are determined in accordance with the rules of the Exchange. Standardized margin trading is only available for listed issues which are selected by the Exchange (standardized margin trading issues and loan trading issues).

The other one type of margin trading is referred to as "negotiable margin trading". Premium charges, payment deadlines, and treatment of rights are determined between the customer and the securities company. Issues eligible for negotiable margin trading are determined by the securities company (excluding issues that fall under the delisting criteria). In negotiable margin trading, unlike standardized margin trading, the securities company cannot borrow the money or stocks required for such transactions from a securities finance company (refer to Question 6).

Some securities companies refer to trading without a payment deadline as "open-ended margin trading".

Some securities companies do not handle negotiable margin trading. Therefore investors are advised to check in advance.

- Q5. Which issues are eligible for margin trading?

-

A5.

Only issues which the Exchange selects out of listed issues (stocks, preferred stocks, ETFs, and REITs) based on the liquidity and other criteria and designated as a standardized margin trading issue or a loan trading issue are eligible for margin trading.

In standardized margin trading, a securities company can borrow money to lend to a buying customer from a securities finance company (refer to Question 6).

In loan trading, a securities company can borrow both money to lend to a buying customer and stocks to lend to the seller from a securities finance company.

As a result, if the securities company is unable to (or does not) procure the stocks on its own to lend to the seller in a margin sale, the company cannot execute margin sales through standardized margin trading.

In addition, some securities companies may restrict issues for which it accepts orders for standardized margin trading based on their internal rules, thus it is necessary to check in advance.

On the other hand, for negotiable margin trading, issues determined by the securities company will be available (excluding issues that fall under the delisting criteria).

- Q6. What is a "securities finance company"?

-

A6.

In margin trading, a customer (investor) deposits customer margin as collateral with a securities company and a customer borrows money to buy stocks or borrows stocks to sell from the securities company (at the end of the deal, the customer settles with the securities company by repaying the borrowed money or returning the borrowed stocks through closing transactions for offsetting or actual receipt/delivery).

In order for a securities company to receive orders from customers for margin trading, it needs to procure money to lend to a buying customer or stocks to lend to a selling customer. In fact, it is not easy for securities companies to perform such procurement on their own.

In this case, it is the securities finance company who plays the role of providing money and stocks required for margin trading (standardized margin trading: refer to question 4) to securities companies. Many securities companies borrow money or stocks required for margin trading from securities finance companies. (This type of trading is referred to as loan trading in which a securities finance company lends money or stocks to the securities companies).

Securities finance companies are required to be granted the relevant license by the Prime Minister under the Financial Instruments and Exchange Act. There are currently two such companies nationwide: Japan Securities Finance Co., Ltd. and Chubu Securities Financing Co., Ltd. Japan Securities Finance Co., Ltd. is the designated securities finance company of TSE.

- Q7. What is a premium charge?

-

A7.

Most securities companies borrow money or stocks required for standardized margin trading from a securities finance company (refer to Question 6). When there is a shortage of stocks because of an increase in the quantity of stocks loaned to securities companies, the securities finance company borrows stocks from other securities firms, institutional investors or shareholders and pays them a fee for the borrowed stocks.

In this procurement, the securities finance company holds an auction to decide the lender of the stock and the fee which the securities finance company pays to the lender.

This fee is referred to as the "premium charge". This charge is transferred by the securities finance company to the securities company, and ultimately to the customer selling the stocks in standardized margin trading by the securities company.

In selling on margin, such cost may be incurred without prior notice and attention should be paid.

- Q8. Is "selling" on margin the same as "short selling"?

-

A8.

In margin trading, a new "sale" is a transaction in which an investor first borrows stocks from a securities company and sells them in the market through a securities company.

On the other hand, "short selling" in general, refers to transactions in which an investor sells borrowed stocks. As such, this term includes margin sales (the method mentioned in the previous paragraph). However, the term also includes other methods of sale where an investor borrows the stock without using margin trading, for example, borrowing from an individual shareholder.

As such, "short selling" is a broader concept which includes "selling on margin".

- Q9. What kind of restrictions and measures are there with regard to margin trading?

-

A9.

The main measures with regard to margin trading include "daily publication" and "regulatory measure (upward revision of customer margin rates)" implemented by the Exchange, and "precaution for the use of stock loans (notice on precaution related to the use of stock loans, etc.)" and "suspension of applications for the use of stock loans (restricting or suspending applications for loan trading)" conducted by a securities finance company.

"Daily publication" and "regulatory" measures implemented by the Exchange are aimed at preventing the market from overheating due to the excessive use of margin trading. In general, these measures are implemented in accordance with the guidelines which are based on numerical criteria.

(Refer to Question 10)

On the other hand, measures such as "precaution for the use of stock loans" and "suspension of applications for the use of stock loans" will be taken by a securities finance company when there is a risk that there may be insufficient stocks held by the securities finance company (refer to Question 6) to lend to the securities firms for margin trading and therefore the procurement may be difficult, and when it is difficult to procure the stocks. (Refer to Question 11)

Please note that the regulatory measures implemented by the Exchange and measures implemented by a securities finance company are implemented by regulatory organizations with different aims.

- Q10. What kind of restrictions and measures are imposed by TSE?

-

A10.

The main measures by TSE on margin trading are "daily disclosure report" and "regulatory measures (upward revision of margin trading deposits)", and they aim to prevent the market from overheating by excessive use of margin trading.

- Daily Publication

"Daily publication" is aimed at preventing excessive use of margin trading by publishing the outstanding margin transactions in issues for which margin trading is active is disclosed on a daily basis (while the outstanding margin transactions for individual issues are disclosed on a weekly basis), thereby alerting investors. The Exchange also identifies issues for which outstanding margin transactions have been continuously increasing among the "Issues subject to Daily Publication" and publishes them as “Issues subject to Special Publication” to inform investors of the situation. - Regulatory Measure

"Regulatory measure (upward revisions of customer margin)" is carried out by raising the rate of customer margin which is normally required for a new margin trade and requiring partial collection in cash with regard to the issues in which there is excessive margin trading. (Some investors refer to this regulatory measure as "additional collateral".) - Guidelines

Daily publication and regulatory measures are implemented and removed in accordance with guidelines (i.e., Guidelines Concerning Upward Revisions of the Ratio of Customer Margin) based on numerical criteria such as for "outstanding margin transactions", "stock price (deviation from 25-day moving average)" or "ratio of margin sales/purchases (ratio of margin sales and purchases to total margin trading volume)".

- Daily Publication

- Q11. I was told by a securities firm that “Margin selling of this loan issue is prohibited. It cannot be sold on margin". What is the content of this restriction?

-

A11.

Some securities companies call this regulatory measure "suspension of margin sales", "prohibition of margin sales" or "margin sale restriction".

In a new sale on margin, a securities company lends stocks to a selling customer, but in many cases it is a securities finance company which provides the stock for lending to the securities company (refer to Question 6).

However, when there is a shortage of stocks and it becomes difficult for the securities finance company to procure them due to increased lending of the stock to securities companies, the securities finance company may stop accepting applications for stock loans from securities companies ("suspension of application for use of stock loans") because there is no stock at hand and the securities finance company is unable to lend it any more (refer to Question 9).

When this regulatory measure is implemented, securities companies which are unable to (or do not) procure the stocks on their own will not accept new sale orders on margin because they are not able to lend them to margin trading customers.

As explained above, if an order for margin sale of a loaned issue is declined, in general, the reason is that the securities company does not have stocks to lend to persons wanting to sell on margin.

Some investors and securities companies refer to this condition as a "restriction" or "prohibition", but it should be noted that it is not a restriction or prohibition implemented by some specific institution (such as a regulatory agency or stock exchange) to restrict or prohibit margin sales.

In addition, in the case where a customer settles his/her long positions by way of actual receipt of purchased stocks, the securities company will have to procure the stock to deliver to the customer. Therefore, when the securities finance company cannot lend the stock to the securities company, the company may decline applications for settlement by way of actual receipt due to the same reason as above.

- Q12. What is outstanding margin transactions?

- A12. Outstanding margin transactions mean the amount of money and stocks borrowed by investors for buying or selling stocks from securities companies which have not been paid or delivered respectively. For outstanding positions reported as outstanding margin transactions, outstanding short positions (stocks loaned by securities companies and borrowed by investors to sell on margin) will be closed through an offsetting purchase or actual delivery, while long positions (funds loaned by securities companies and borrowed by investors to buy on margin) will be offset by selling in the market or actual receipt of the stocks.

- Q13. Why is there a difference between the figures for outstanding margin transactions disclosed by TSE and the figures for outstanding funds or stocks loaned by the securities finance company (Japan Securities Finance Co., Ltd.)?

-

A13.

This is because the content of "outstanding margin transactions" released by TSE differs from that of Japan Securities Finance Co., Ltd. "Outstanding margin transactions" disclosed by the Exchange are all outstanding loans (outstanding positions) for margin transactions executed on the TSE market.

On the other hand, "outstanding loans (loaned funds/stocks)" which Japan Securities Finance Co., Ltd. releases only shows the outstanding loans of funds and stocks which securities companies borrow from Japan Securities Finance Co., Ltd.

Therefore, since the report disclosed by Japan Securities Finance Co., Ltd. does not include outstanding loans for standardized margin trading in which a securities company borrows money or stocks for lending to its customer on their own instead of borrowing from Japan Securities Finance Co., Ltd., and those pertaining to negotiable margin trading, the numbers released by the two institutions are different (TSE's "outstanding margin transactions" are always equal to or larger than the "outstanding loans (loaned funds/stocks"). (For the difference between standardized margin trading and negotiable margin trading, please refer to Question 4)

- Q14. How is an account for margin trading pertaining to foreign stocks handled?

-

A14.

In margin trading of foreign stocks, etc, in accordance with the provisions of the Agreement for Setting up Margin Trading Account (Section 1), all transactions between a customer and a financial instruments business operator such as delivery and receipt of cash, securities, customer margin are carried out through a margin account. Therefore, regardless of whether or not a foreign securities account has been opened, transactions are executed through the margin account.

However, when a customer closes his/her long positions in margin trading (i.e., buying on margin) by way of actual receipt, since such purchased stocks will be transferred from a margin account to a foreign securities account, a foreign securities account must have been opened beforehand. Regarding a foreign securities account, payment of dividend or handling in cases where rights such as subscription warrants are granted, please refer to the following page. Please note that even if you already have a foreign securities account, margin transactions pertaining to foreign stocks will be processed in the margin account, as explained above.(Note)- ・In order to open a foreign securities account, it is necessary to submit an application for opening an account to a financial instruments business operator and receive an "agreement for establishment of foreign securities accounts". Rights and obligations for investors as well as financial instruments business operators in foreign securities transactions are prescribed in this agreement.

- ・Although foreign stock trading is basically the same as that for domestic stock trading, when investing in foreign stocks, investors are advised to pay attention to risks peculiar to foreign stocks, such as foreign exchange risk or country risk.

When-Issued Transactions

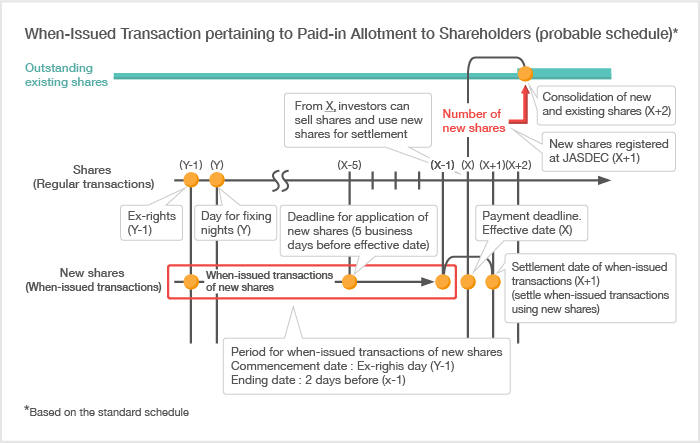

- Q1. What is a when-issued transaction?

-

A1.

A when-issued transaction is trading conducted before new shares are issued when there is an issue of new shares in a paid-in capital increase by allotment to shareholders*. Trading can be conducted from the ex-rights date to the day which is 2 business days prior to the registration of such new shares at Japan Securities Depository Center (JASDEC). Regardless of the day of execution of a when-issued transaction, all such transactions are settled on the 3 business day counting from the last day of the period when when-issued transactions can be made. As such, someone who executes a when-issued transaction early and another person who executes another when-issued transaction later in the period will have to wait for different lengths of time till their respective trades are settled.

In addition, if an investor sells and buys the same amount of shares in the same issue, settlement can be carried out by deposit or receipt of net gain or loss.

While the trading rules for when-issued transactions are basically the same as regular transactions, there are some very different areas such as the Customer Margin scheme (see Question 8). Before conducting a when-issued transaction, investors will also need to submit the "Agreement on Entrustment of When-Issued Transactions" (see Question 7) which specifies the rights and obligations between the investor and the securities company during the period when such transactions can be made.

- Q2. Why do people conduct when-issued transactions?

- A2. When a listed company conducts a paid-in capital increase by allotment to shareholders, and new shares are issued, shareholders who are allotted such new shares will bear the risk of fluctuations in the stock price until such new shares come into effect. The purpose of when-issued transactions is to provide a means to trade such shares to allow these shareholders to mitigate this risk.

- Q3. When do when-issued transactions actually take place?

-

A3.

In order to list, by when-issued transactions, new shares which are issued due to a paid-in capital increase by allotment to shareholders, the issuing company will apply for listing such shares to TSE, and TSE will then check based on certain criteria before approving the listing.

Stocks and preferred equity investment securities etc. are eligible for such transactions.

(Outline of criteria for handling listing by when-issued transactions)

Domestic stocks and preferred equity contribution securities- The registration, etc. pursuant to Article 4, Paragraph 1 of the Financial Instruments and Exchange Act has come into effect.

- The number of shares is at least 4,000 units.

- Where the state of share distribution after listing is deemed to not be extremely poor.

- Q4. Will there be when-issued transactions every time there is a paid-in capital increase by allotment to shareholders?

- A4. When-issued transactions are examined and approved only if there is an application by the listed company (see Question 3). If the listed company does not apply or does not satisfy certain criteria, when-issued transactions will not be allowed. This means a paid-in capital increase by allotment to shareholders does not always mean that when-issued transactions will be available.

- Q5. What is the schedule of when-issued transactions?

-

A5.

The period for when-issued transactions is from the ex-rights date to the day which is 2 business days prior to the day such new shares are newly registered at JASDEC. In addition, all such transactions are settled on the 3 business day counting from the last day of the period.

A summary of the schedule for when-issued transactions is as follows.

Summary of Schedule for When-Issued Transactions- Start of Period : Ex-rights date(Where TSE deems necessary, this may be on or after the ex-rights date.)

- End of Period : 2 business days prior to the day the new shares are registered at JASDEC

- Settlement Day : Last trading day +2

- Q6. How does a when-issued transaction work?

-

A6.

Investors will need to indicate that an order is a when-issued transaction. Trading is conducted in the exactly same way as regular transactions: market or limit orders are matched in auction order books of individual issues using the Itayose or Zaraba method (the trading unit and tick size is also the same as that in regular transactions; however, the price limit on bids and offers will be that for the existing shares on the day). Some securities companies do not handle when-issued transactions, therefore investors are advised to check in advance. Please also be informed that the issue code for new shares will be a five-digit code with "1" appended to the end of the four-digit code for existing shares (e.g., new Sony shares: 67581).

The major differences from regular transactions are that there is a specified trading period, a long duration until settlement, payment or receipt of such gain or loss for settlement of buying and selling identical amount of shares in the same issue during this period (An investor may sell in a when-issued transaction even if he/she is not allotted the new shares. However, in this case, there must be a purchase or other act before the settlement date, so that there are no issues in relation to settlement).

To ensure that settlement is carried out and excessive speculation is reined in, when carrying out a when-issued transaction, an investor must deposit to the securities company a predetermined Customer Margin (at least 30% of execution value) between the day the trade is executed (T) until time the securities company decided on the third day counting from the day of the trade (T+2) (see Question 8). During the trading period, there is a need to clarify the rights and obligations between the investor and the securities company. As such, before carrying out a when-issued transaction, investors are required to submit to the securities company, the "Agreement on Entrustment of When-Issued Transactions" which specifies such rights and obligations.

Please also note that when-issued transactions are not available in ToSTNeT trading.

- Q7. What is the content of the "Agreement on Entrustment of When-Issued Transactions"?

-

A7.

To entrust a when-issued transaction order to a securities company, an investor must first fill in the required items in the "Agreement on Entrustment of When-Issued Transactions", sign or attach a seal to the agreement and submit it to the securities company.

The duration of the trading period for when-issued transactions and the period when rights and obligations occur between an investor and his/her securities company are long. The agreement contains content on what must be agreed on such as liability for damages during failure to fulfill obligations aimed at clarifying rights and obligations that occur during the trading period beforehand. Therefore, investors are advised to thoroughly read and sufficiently understand the content of the agreement before carrying out a when-issued transaction.

As a general rule, agreements fall under "Contracts forming the basis of continuous transactions (keizoku-teki-torihiki no kihon to naru keiyakusho)" prescribed in the law on stamp duty in Japan, and stamp duty of 4,000 yen applies to each copy. However, stamp duty does not apply to contracts which have a contractual period of three months or less and also do not contain a clause concerning renewal of the contract.

Download the "Agreement on Entrustment of When-Issued Transactions" here.

Agreements for setting up accounts

- Q8. What is "Customer Margin"?

-

A8.

- Customer margin

A when-issued transaction is conducted over a long period of time. To ensure that settlement is carried out and excessive speculation is reined in, when carrying out a when-issued transaction, an investor must deposit to the securities company a predetermined Customer Margin between the day the trade is executed (T) until time the securities company decided on the third day counting from such day (T+2). The required amount of Customer Margin is specified in the "Cabinet Office Ordinance concerning transactions prescribed in Article 161-2 of the Financial Instruments and Exchange Act as well as margins for such transactions" and the rules of TSE as at least 30% of the execution value (i.e., execution price x number of shares bought/sold). Some securities companies may set margin ratios at more than 30%. If the market is likely to overheat due to excessive use of when-issued transactions, in order to rein in the use of such transactions, the Customer Margin ratio may be raised through an amendment of the Cabinet Office Ordinance or at the discretion of TSE. In such cases, the required Customer Margin would be the amount obtained by multiplying the execution value after the ratio is raised. - Securities in lieu of money

Securities may be deposited in substitute of cash for Customer Margin. Such securities are known as "securities in lieu of money". The types of securities eligible for use as securities in lieu of money are as follows:Since the price of these securities may fluctuate or even fall after they are deposited, the security is valued by applying a certain rate to the price of the security in the market. The rate is fixed according to type of security, e.g., 80% for stocks. In addition, it is specified in the rules that "the substitution price of securities in lieu of money shall not exceed the value obtained by multiplying (1) the market price on the day prior to the day the Customer Margin is deposited by (2) the haircut rate (i.e., a securities company may not value securities in lieu of money above the value obtained by multiplying the market price by the rate specified by the Exchange)." As such, a securities company may apply a 60% rate to stocks or a 60% rate to a certain issue.- Listed stocks

- Japanese government bonds, municipal bonds, and government guaranteed bonds

- Corporate bonds of listed domestic companies and convertible bonds

- Corporate bond investment trusts and equity investment trusts

- ETFs and REITs

- Other securities specified by cabinet office ordinances and the Exchange

Haircut Rate by type of Securities in lieu of Money

Type of Securities in lieu of Money eligible for Customer Margin Rate (1) Stocks listed on a domestic securities exchange 0.80 (2) Japanese government bonds 0.95 (3) Municipal bonds (limited to those for which an original underwriting agreement for the issuance was concluded by a domestic or foreign securities company) 0.85 (4) Bonds issued by corporations based on special laws (also known as special bonds)

•Bonds whose principal redemption and coupon payment are guaranteed by the government

•Other such bonds0.90

0.85(5) Corporate bonds listed on a domestic securities exchange

(excluding bonds with subscription warrants (including bonds with subscription warrants that are subscribed and allotted at the same time, and in addition, traded together; the same applies hereinafter) and exchangeable bonds; the same applies hereafter) or corporate bonds issued by a company whose shares are listed on a domestic securities exchange, and in addition, which are issued by a company other than a foreign juridical person (limited to those for which an original underwriting agreement for the issuance was concluded by a domestic or foreign securities company)0.85 (6) Bonds with subscription warrants listed on a domestic securities exchange or bonds with subscription warrants issued by a company whose shares are listed on a domestic securities exchange, and which are issued by a company other than a foreign juridical person (limited to those for which an original underwriting agreement for the issuance was concluded by a domestic or foreign securities company) 0.80 (7) Exchangeable bonds listed on a domestic securities exchange (limited to those for which an original underwriting agreement for the issuance was concluded by a domestic or foreign securities company) 0.80 (8) Foreign government bonds listed on a domestic securities exchange 0.85 (9) Foreign municipal bonds listed on a domestic securities exchange 0.85 (10) International Bank for Reconstruction and Development yen-denominated bonds 0.90 (11) Asian Development Bank yen-denominated bonds 0.90 (12) Yen-denominated foreign bonds issued by a foreign juridical person (limited to those listed on a domestic securities exchange) other than issuers of bonds in (8) through (11), 0.85 (13) Investment trust beneficiary certificates and investment securities (limited to those listed on a domestic securities exchange and those whose market price for the previous day is published by The Investment Trusts Association, Japan)

•Investment trust beneficiary certificates of bonds

•Others0.85

0.80(14) Beneficiary certificates of a beneficiary certificate issuing trust (limited to those listed on a domestic securities exchange) 0.80 - Customer margin

- Q9. Why is there a need to deposit Customer Margin?

-

A9.

Since the time from execution to settlement of a when-issued transaction is long, deposit of Customer Margin becomes significant as a means of ensuring that settlement by an investor is secured.

It also combines an aspect aimed at reining in excessive speculation with restrictions on Customer Margin for when-issued transactions and its ratio. In a when-issued transaction, the portion of sales and purchases in equivalent amounts of the same stock can be settled through netting. This enables investors to trade more than the amount of funds they have on hand, and also makes speculative abuse possible. Excessive speculation through when-issued transactions can be reined in by changing the Customer Margin ratio.

In this way, depositing Customer Margin has significance as collateral, and also is a means of ensuring that the use of when-issued transactions is used appropriately. This is achieved by not giving securities companies complete freedom on Customer Margin ratios and specifying certain limits in laws and regulations as well as TSE rules.

- Q10. Can I withdraw Customer Margin or use it for other purposes?

-

A10.

As a general rule, Customer Margin that has been deposited cannot be withdrawn or used as Customer Margin for a new when-issued transaction before settlement of the corresponding when-issued transaction is completed.

However, if an investor has deposited more than the required amount, he/she can withdraw such excess Customer Margin or use it for other purposes. The following explains how the amount of Margin that can be deposited or used for other purposes is calculated.

The required amount of Customer Margin is constantly changing. For example, even if an investor initially deposits 1 million yen, if losses of 300,000 yen are incurred due to subsequent price fluctuation in the shares bought or sold in a when-issued transaction, the substantial value of the deposited Customer Margin will be 700,000 yen, i.e., 300,000 yen deducted from the initial 1million yen.

If securities in lieu of money are deposited in place of Customer Margin, the value will change with fluctuations in the price of the deposited securities. First, the total value of the deposited margin will be calculated (i.e., substantial collateral value of the Customer Margin). The calculation is specified in the "Cabinet Office Ordinance concerning transactions prescribed in Article 161-2 of the Financial Instruments and Exchange Act" as well as Brokerage Agreement Standards of the Exchange.

Total amount of deposited Margin = Total amount of Customer Margin currently deposited-Amount of unrealized losses due to changes in market prices and offsetting transactions - All liabilities concerning when-issued transactions that should be borne by the customerFor example, a customer deposits 150,000 yen as Customer Margin for buying 5,000 shares at 100 yen in a when-issued transaction for an issue. This is equivalent to 30% of the execution value. The same customer then sells 2,000 shares at 110 yen and 1,000 shares at 90 yen for the same issue. At the time just before settlement, the stock price is 80 yen. The total amount of deposited Margin will be calculated as follows (simplified calculation which omits other fees such as brokerage commission).- Total amount of Customer Margin currently deposited: For securities deposited in lieu of money for Customer Margin, the amount converted into money by multiplying the (1) market price(s) on the day prior to the day of calculation by (2) the rate(s) specified for each type of security.

- Amount of unrealized losses due to changes in market prices and offsetting transactions: Amount of net losses including losses due to change in the price of the security for the when-issued transaction, as well as (1) gains due to change in the price of the security for the when-issued transaction and gains from offsetting transactions deducted from (2) losses from offsetting transactions (net gain is not included in calculations).

- Offsetting transaction: This refers to purchases and sales of shares in the same issue to offset a short or long position in when-issued transactions. For example, this means buying 2,000 shares in a when-issued transaction when selling 5,000 shares in a when-issued transaction.

- All liabilities borne that should be borne by the customer: This includes costs that must be borne by the customer such as brokerage commission.

Total amount of deposited Margin = 150,000 − {(Loss: 40,000+10,000) − (Gain: 0+20,000)} *1 = 120,000 yenThe amount available for withdrawal or appropriation to Margin will basically be the amount in excess of the amount arrived at by deducting (1) the required amount of Customer Margin (30% of execution value) from (2) the total amount of Customer Margin obtained from the above calculation. This amount will be available for use as Customer Margin for new when-issued transactions.- Losses due to changes in market prices *2 : (100-80) yen ×{ 5,000-(2,000+1,000)} shares = 40,000 yen

- Losses due to offsetting transactions *2: (100-90) yen × 1,000 shares = 10,000 yen

- Gains due to changes in market prices *2 : 0 yen

- Gains due to offsetting transactions *2 : (110-100) yen × 2,000 shares = 20,000 yen *1 If the amount in { } is net gain (i.e., gains exceed losses), this is not included in calculations.

*2 If multiple trades or multiple issues were traded, they will be included accordingly.

Amount available for withdrawal or appropriation to Margin = Total amount of deposited Margin − Amount equivalent to 30% of execution value of when-issued transaction Execution value of when-issued transaction: Execution value at the time when the when-issued transaction is carried out. If there were multiple trades or multiple issues, they will be included accordingly. When using for appropriation, this shall exclude the execution value for offsetting transactions in the same issue.

If there are offsetting transactions in the same issue, the Customer Margin for the offset amount may be returned to an investor. However, when unrealized losses due to these offsetting transactions occur, the investor will have to deposit money equivalent to the amount for such losses.

Furthermore, when the settlement date for when-issued transactions arrives, the deposited Customer Margin can be withdrawn to be used for such settlement. However, if an investor makes when-issued transactions in multiple issues, when the first of the settlement dates for multiple when-issued transaction issues arrives, only the amount in excess of the required amount of Customer Margin for all when-issued transactions by the investor can be withdrawn to be used for settlement.

For the same case, an investor can withdraw and use all Customer Margin for settlement of this issue based on the condition that all of the purchased stocks or sales proceeds received from settlement of the first when-issued transaction issue are deposited as Customer Margin (limited to cases where the total amount after Customer Margin is deposited exceeds the required amount of Customer Margin for all other when-issued transactions).

Please note that even if there is unrealized gains from price gains in the new shares purchased or offsetting transactions before a when-issued transaction is settled, investors cannot withdraw the amount for this amount gained and use it for Customer Margin for a new when-issued transaction (see Question 11).

- Q11. If, based on calculations, there is a gain before settlement, can this be withdrawn or used for other purposes?

-

A11.

As mentioned in the formula for calculation of the total amount of Customer Margin in Question 10, even if there is unrealized gains before settlement, the amount equivalent to that amount gained cannot be included in the actual amount of Customer Margin deposited (losses from other when-issued transactions may be deducted). As such, an investor cannot withdraw the amount equivalent to this amount gained and use it for Customer Margin for a new when-issued transaction.

The reason for this rule is that unrealized gains due to changes in market prices is only temporary valuation (i.e., subsequent market conditions may change), and there would be no actual gain before settlement is completed. Despite such considerations, allowing investors to withdraw or use such unrealized gains due to temporary valuation for appropriation would destabilize the scheme in place for when-issued transactions where Customer Margin of at least a certain amount is deposited as collateral. This would also invite even more excessive speculation.

- Q12. What is "additional margin"?

-

A12.

"Additional margin (oisho)" means "additional deposit of Customer Margin" submitted to a securities company when unrealized losses are incurred due to offsetting transactions or changes in the market such as when the price of shares purchased in when-issued transactions fall or when the prices of shares sold in when-issued transactions rise.

Deposit of additional margin is made up of (1) "Voluntary deposit for unrealized losses", and (2) "Mandatory deposit when falling below the maintenance ratio".- Voluntary deposit for unrealized losses

As explained in the calculation of the total amount of deposited Margin, if there are unrealized losses due to changes in the market, the substantial value of the deposited Customer Margin falls.

In order to maintain the value of collateral in the Customer Margin from the perspective of protecting account receivables, even if the case does not fall under the maintenance ratio provision in (2) below, a securities company may require its customer to deposit additional Customer Margin equivalent to such losses. - Mandatory deposit when falling below the maintenance ratio

- Maintenance ratio

If the value of the initially deposited Customer Margin decreases due to an increase in the amount of unrealized losses or a decline in the valuation of the securities deposited in lieu of money, the value of the initially deposited Customer Margin may be insufficient as collateral.

However, in the course of maintaining the collateral value of the initially deposited Customer Margin, there will be frequent operational procedures between a securities company and its customers due to the delivery and receipt of Customer Margin between them as and when the day-to-day price changes in the market, where there are unrealized losses, or when the valuation of securities deposited in lieu money change.

In order to prevent such a situation, investors are not required to deposit additional margin until the total value of the deposited Customer Margin falls below a certain ratio of the execution value, and where this falls below this ratio, from the perspective of protecting accounts receivable of the securities company, the Brokerage Agreement Standards of TSE specify that it must be maintained at a minimum ratio of the execution value. - Deposit deadline

If the total amount of deposited Margin falls below 20% of the execution value of a when-issued transaction, the customer must deposit additional Customer Margin to maintain this at 30% or above by time the securities company decided on the day after the following day it falls below 20%. In addition, once a call for additional Margin occurs, even if the total amount of deposited Margin reaches at least 20% due to price changes in the market before additional margin is deposited, additional margin must still be deposited by the initial deposit deadline. - If additional margin is not deposited

If an investor does not deposit additional margin, for settling the relevant when-issued transaction, the securities company may choose to sell (long position) or buy (short position) for the customer's account. Other specific measures customers must agree to before conducting when-issued transactions are described in the "Agreement on Entrustment of When-Issued Transactions".

- Maintenance ratio

- Voluntary deposit for unrealized losses

- Q13. Can I substitute securities deposited in lieu of money for Customer Margin?

-

A13.

Substitution of Customer Margin means simultaneously exchanging money or securities deposited in lieu money as Customer Margin with money or securities whose value is at least equivalent to such amount.

As long as the above condition is satisfied, substitution of Customer Margin is possible regardless of the size of the amount of deposited Margin (this means that it can be done even when the total amount of deposited Margin is less than 20% of the execution value).

Other than depositing money or securities in lieu of money when substituting Margin, customers can also choose to acquire money or stocks from existing deposited Margin. In other words, an investor may sell securities deposited in lieu of money for Customer Margin and deposit the proceeds from such sales as Customer Margin, or deposit the stocks bought using the proceeds from such sales as Customer Margin.

Investors are advised to note that if the newly deposited Margin, etc. falls below the valuation of the securities initially deposited in lieu of money, they are required to separately deposit money or securities in lieu of money before the day of the substitution is made to make up for this difference. Otherwise, substitution will not be allowed.

- Q14. What is Trading Margin?

-

A14.

Retail investors are not directly affected by Trading Margin. Trading Margin is collateral for when-issued transactions deposited by securities companies. They are required to deposit Trading Margin by a fixed deadline (by noon of the fourth day (T+3) counting from the day a trade is executed (T)) to the clearinghouse (Japan Securities Clearing Corporation (JSCC)) based on the net amount of sales/purchases for each issue.

This amount shall be at least the amount obtained by multiplying (1) 0.10 of the closing price on the day of commencement of when-issued transactions by (2) the net amount of shares bought or sold. Securities designated by the clearinghouse may be deposited in lieu of money. For securities companies which do not hold clearing qualifications, TSE rules require them to deposit Trading Margin to clearing participants (i.e., those who hold JSCC clearing qualifications).

- Q15. How is a when-issued transaction settled?

-

A15.

Regardless of when a when-issued transaction is executed, all when-issued transactions are settled on the 3 business day counting from the end of the period when-issued transactions can be carried out (last trading day + 2 business days). As such, the duration until settlement varies depending on the trade execution date. As a general rule, an investor must deliver the new shares (if selling) or pay the corresponding consideration (if buying) to his/her securities company by 9:00 a.m. on the settlement day.

For the portion of trades of equivalent amounts of shares bought and sold in the same issue, settlement can be conducted by netting gains or losses. This is a distinctive aspect of when-issued transactions.

For example, during the trading period, an investor buys 1,000 shares at 100 yen and sells 500 shares at 120 yen. During settlement, as a result of the offset, he/she shall pay 40,000 yen (i.e., 120 yen x 500 shares − 100 yen x 1,000 shares) and receive 500 shares (i.e., 1,000 shares − 500 shares).

- Q16. Can I use existing shares for settlement of a when-issued transaction?

-

A16.

When an investor sells in a when-issued transaction, even if he/she holds the existing shares, they cannot be used for settlement.

When-issued transactions are intended for trading only new shares which have not come into effect. Even though existing shares are shares of the same company, if they can be used in settlement of when-issued transactions, the scope of when-issued transactions would then include existing shares, and may give rise to excessive speculation. As such, only new shares can be used for settling when-issued transactions.

- Q17. When can new shares be sold as existing shares?

-

A17.

New shares are consolidated with existing shares on the day following the day they are registered at JASDAC (the business day following the settlement day of when-issued transactions). Since investors who are holders of new shares are able to use them for settling trades in existing shares, they will be able to sell the new shares in the market for existing shares from 2 business day prior to the day of consolidation of new and existing shares.

Please note that the handling of new and existing shares may vary depending on the securities company. Investors are advised to check with the relevant securities company when intending to sell new shares.

- Q18. Where can I get information on when-issued transactions?

-

A18.

The list of issues for which when-issued transactions can be made is available on the TSE website. This list contains issues and the schedule for when-issued transactions. In addition, investors can check the stock price of the new shares via the Stock Price search feature on the TSE website or in relevant sections of newspapers ("new" may be appended to the name of such stock, e.g., Sony new).

Information on regulatory measures such as raising the Customer Margin ratio or imposing restrictions on deposits of securities in lieu of money as Customer Margin are published on the TSE website and other relevant sources.

- Q19. Are there any other matters needed to be aware of?

- A19. Handling of aspects such as the Margin ratio or deposited assets may vary depending on the securities company. Other than this, when TSE deems that the trading situation of when-issued transactions is abnormal or is likely to become abnormal, TSE may implement measures such as raising the Customer Margin ratio, imposing restrictions on the deposit of securities in lieu of money, or on when-issued transactions.